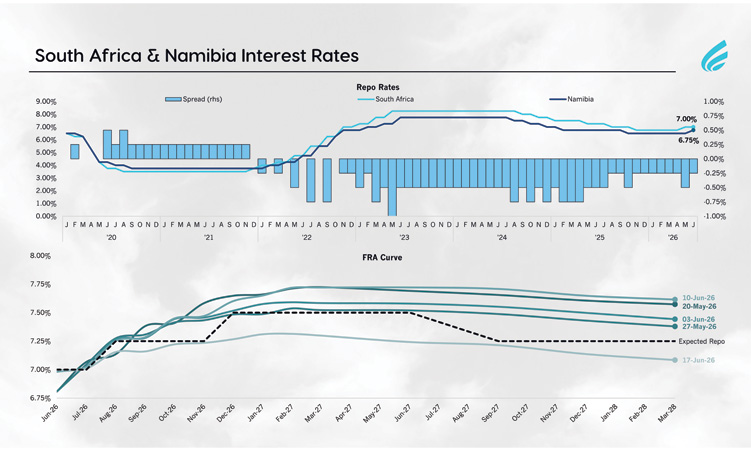

THE Bank of Namibia’s Monetary Policy Committee raised the repo rate by 25 basic points to 6.75% on 17 June, following the South African Reserve Bank’s 25 bps hike in May.

For Namibia, the decision was largely a response to South Africa, as a large negative interest-rate spread between the two countries could encourage capital outflows and place pressure on foreign reserves and the currency peg.

The broader reason behind the shift to a more restrictive monetary policy stance is the inflation risk created by the Middle East conflict.

Central banks are trying to get ahead of the shock before it becomes more broad-based and embedded in inflation expectations.

Even though higher rates cannot solve the supply-side issues driving the initial price pressure, they can dampen demand and help prevent a temporary oil-price shock from turning into a broader inflation problem.

However, there is a strong argument that both central banks may have moved too hastily.

The US Federal Reserve and the European Central Bank both kept rates unchanged.

The global backdrop has also shifted quickly in a more positive direction.

A United States-Iran peace framework now appears more realistic, with both sides expressing confidence in a deal, and oil prices have almost fallen back to pre-conflict levels.

If the agreement holds and shipping normalises, the inflation impulse that triggered the hikes could fade relatively quickly.

However, there will still be issues around global oil stockpiles even if peace were to hold, and peace is not a certainty.

Israel appears less committed to de-escalation, and continue to strike Hezbollah in Lebanon to disrupt proceedings.

That said, markets appear to expect conditions to normalise relatively rapidly.

This can be seen not only in the oil price, but also in South African interest-rate expectations.

South African interest-rate expectations can be seen through the FRA curve.

A Forward Rate Agreement, (FRA), is a short-term interest-rate derivative that effectively shows where the market expects short-term interest rates to be in the future.

The chart shows that markets still expect one more rate hike before the end of the year, before cuts re-emerge in ‘27.

However if the peace deal does hold the latest hike may be all we see of its nature for the foreseeable future.

– Oliver Diggle is an economist at Cirrus.