The 2025/2026 financial year (FY) mid-term budget revealed a flatter revenue path for the fiscus.

Total collections for FY 2024/2025 are revised down to N$89.1 billion and FY 2025/2026 to N$89.4 billion, a rise of just 0.4% year-on-year, with a further N$18.3 billion shaved off the following two years.

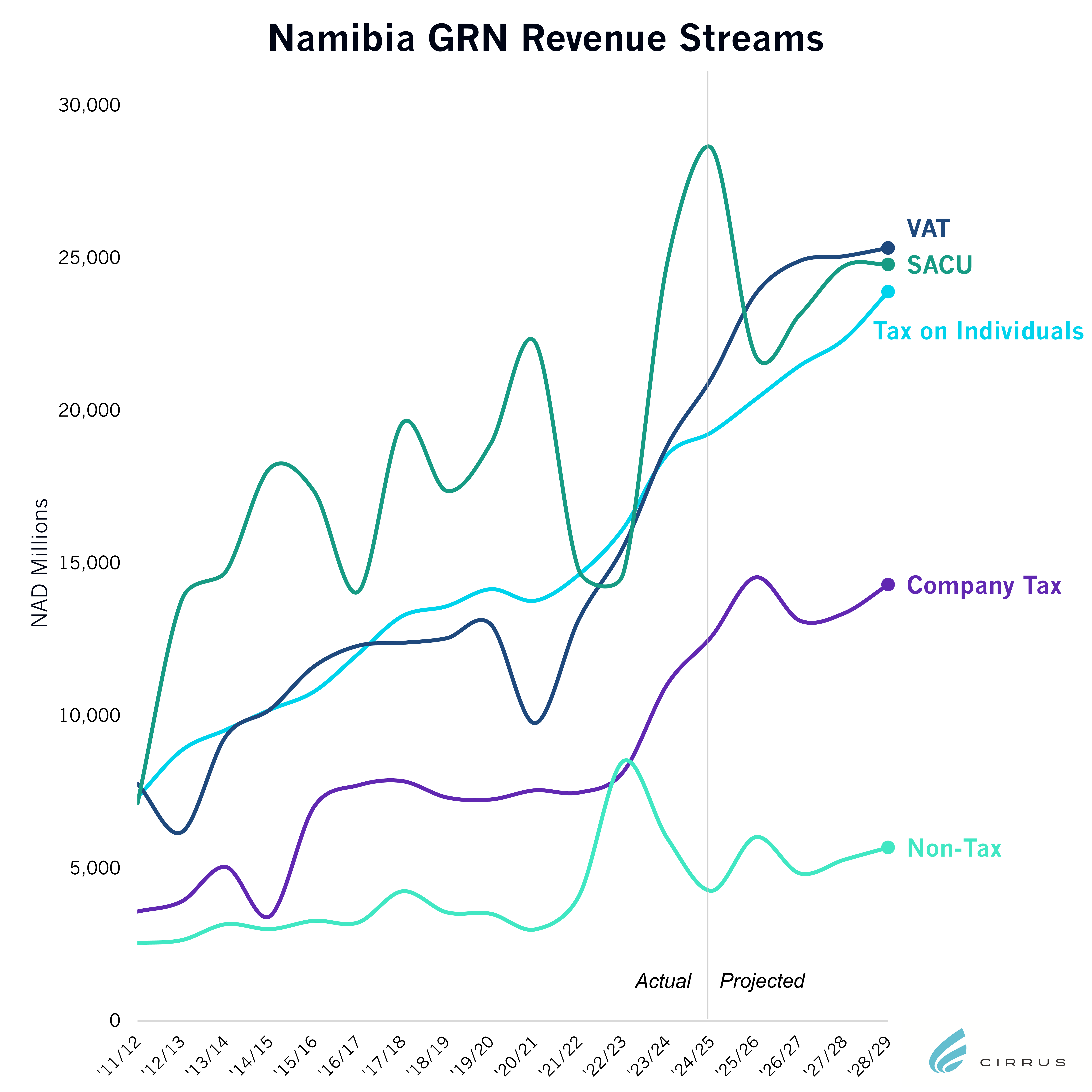

The downgrades are led by value-added tax (VAT), with softer expectations for personal income tax and the Southern African Customs Union (Sacu) compounding the effect. Non-tax revenue is also trimmed across the horizon.

VAT is now the anchor line in both level and forecast risk. Domestic taxes on goods and services reached N$21.1 billion in FY 2024/2025 on firmer consumption and better administration, but the outlook is deliberately flat. Relative to prior forecasts, cuts across the medium-term expenditure framework are material. Rising refunds and the lack of a credible consumption catalyst justify this caution.

Sacu receipts, a major but volatile contributor, remain elevated versus pre-2024/2025 levels, though the treasury has pared back the outlook in line with slower regional growth.

Company tax is the outlier on optimism. The projection lifts FY 2025/2026 to N$14.5 billion, driven by non-diamond mining on stronger Namibia-dollar metals prices and higher volumes in gold and uranium.

Non-diamond mining taxes then taper in the outer years, yet diamond company tax is pencilled to rebound to near N$1 billion by the end of the medium-term expenditure framework. Given softer diamond prices, lower output and revised-down royalties, this looks optimistic.

Personal income tax growth is moderated as the post-pandemic rebound and administrative gains fade. Sustained growth will require faster private-sector job creation and wage gains. On current signals that impulse is weak, so a flatter personal income tax path is the realistic assumption.