Trump’s tariffs were meant to restore American manufacturing pride. Instead, they have shaken up global markets and handed unexpected momentum to emerging economies.

When Donald Trump rolled out tariffs earlier this year, he framed it as a matter of survival. Foreign trade practices, the White House argued, had become a “national emergency” for the US. This was his weapon of choice to shore up America’s economic position and protect workers.

But tariffs are slippery things, Sangeeth Sewnath, managing director of Americas at Ninety One, pointed out at the Morningstar Investment Conference in Cape Town recently. “The point of tariffs serves two purposes. It’s either protection or it’s leverage. At the moment, you will see that it’s a lot more leverage than it is protection.”

International economist at Morningstar Investment Management, Grant Slade, warned that these policies were unlikely to achieve their intended goals. Instead, he predicted a “stagflation-style” scenario where slowing consumer demand and supply-side disruptions diverged, leaving the US economy facing weaker growth and higher prices in the coming quarters.

Sewnath sees this approach as no surprise. After a year of living and working in the US, he has seen this mindset up close. “In the US, they would prefer strong and wrong over weak and right,” he said. That instinct is supported by US exceptionalism, which, he stressed, is not a concept but rather “how they live and what they believe”.

Unintended consequences

The irony of Trump’s tariff blitz is how it has strengthened rivals. In China, the trade war has reinforced the Communist Party’s grip on power and nudged neighbours like Japan and South Korea into closer cooperation with Beijing, according to Liang Du, CEO at Prescient Private Fund Management in Shanghai.

He said Trump’s immigration clampdown has sent a wave of skilled scientists and engineers back home. “Historically, the best and brightest would go overseas, especially in the US, to study. Typically, they would stay and create companies and grow innovation in the US. In the last two terms, that has dramatically started to change.

“Now what’s happening, you have this witch hunt going on in US academia and innovation, where Chinese scientists and engineers are being kicked out of the US. Usually, they won’t even go back to China, but they’re probably pretty angry. Now they’re all coming back to China, taking a big pay cut, and driving a lot of innovation. For the last five years, China is the only other place, other than the US, with mega tech corporations, with AI, with advanced engineering.”

With a wry grin, he added: “What Trump has done for China, China could not do for itself in decades.”

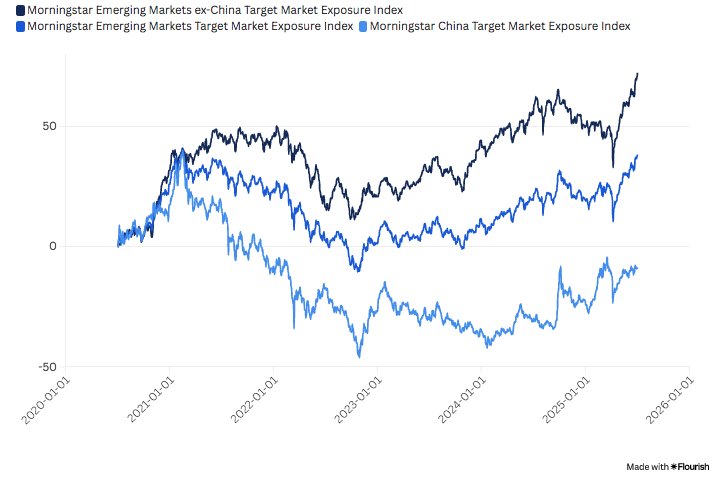

Performance of Morningstar EM Indexes over five years

India has also found itself in a sweet spot. Market-opening reforms under Prime Minister Narendra Modi have delivered strong market returns, while low labour costs and rising productivity make it an attractive alternative manufacturing base, Allan Gray portfolio manager Pieter Koornhof, said.

“The other important competitive advantage for India is that it isn’t China. What we’ve seen is [that] from the Covid pandemic, there’s trade tension between China and the US, this sort of geopolitical rivalry for global dominance. India isn’t part of that.”

By contrast, Europe has absorbed the trade shock with fewer supply-side disruptions but faces its own long-running challenges: an ageing population, high taxes and a shrinking workforce that make consistent growth hard to sustain, Slade said.

Emerging markets finding their moment

Since the end of World War 2, the US market has dominated global trade. In 2025, analysts see what Michael Dodd, senior fund analyst at Morningstar Investment Management, called “a bit of a turning point”.

Fund managers are more overweight in emerging markets than at any time in the past two years, Dodd said, and confirmed that “South Africa has not been left out of that”.

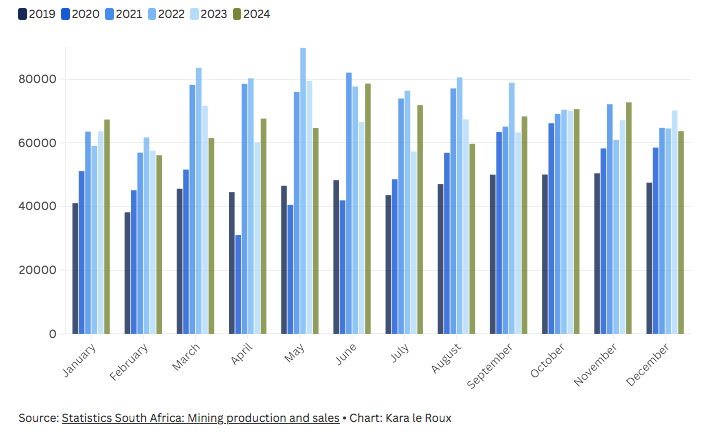

This local rally has been most visible in resources. “South Africa has benefited from its rotation between emerging markets,” said Koornhof, pointing to the mining sector as this year’s real winners. Campbell Parry, commodities and natural resource analyst at Investec, noted that gold stocks had doubled their share of the local index since January, while platinum group metals had also climbed.

South African mineral sales at current prices (R million)

The rest of the South African economy, however, looks less lively. According to Koornhof, banks and retailers are still limping under the weight of low growth and squashed post-election hopes. South Africa’s overall share of emerging markets keeps shrinking, a “fading star” as Parry calls it, with capital being drawn to faster-growing peers like Taiwan and China.

Even so, Koornhof believes that South African businesses remain resilient.

Hardened by State Capture, load shedding and a pandemic, they are leaner, meaner, and still standing. Low expectations, he argues, mean that even small improvements can deliver returns if the government and the private sector move in step.

How investors are adapting

The Eskom Pension and Provident Fund (EPPF) is among the local investors restructuring its portfolios. Its offshore exposure now reaches 45%, says EPPF chief investment officer Sonja Saunderson, while infrastructure and unlisted ventures at home are getting more attention.

Saunderson emphasised that there were “a lot of these happening in South Africa in the unlisted space,” including “good technical, technological and digital advances [in] search engines that Silicon Valley is really keen on buying”.

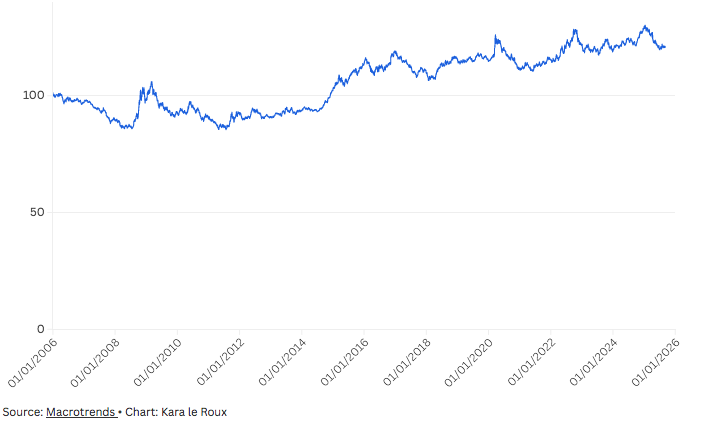

Globally, Sewnath sees a weaker dollar under way. He predicts it could last 15 to 18 years, which would provide a strong tailwind for emerging markets.

US dollar index 2006-2025

Liang believes that China should remain part of any diversified portfolio. Despite concerns about the country’s property market, he said that the country’s low correlation with both the US and South African markets makes it a useful diversifier. A weighting of 10% to 20% would be enough to matter without overexposing the portfolio, he advised.

Sewnath also urged investors to keep perspective. “I think volatility and turbulence is a feature, it is not a bug. It’s not going to last forever. So you’ve got to make sure you’re building the right portfolios for the long term.” DM